The 1/10th Rule For Car Buying Everyone Must Follow

If you’re looking for a car buying rule, let me introduce you to the 1/10th rule for car buying. The 1/10th rule will help you spend responsibly, reduce your car ownership stress, and boost your net worth over time.

Back in 2009, I watched in horror as a total of 690,000 new vehicles averaging $24,000 each were sold under the Cash For Clunkers program.

The government’s $4,000 rebate for trading in your car ended up hurting hundred of thousands of people’s finances instead. With a median household income of only around $50,221 at the time, spending $24,000 on a new car was clearly too much.

Instead of buying a $24,000 car in 2009, you could have invested the $24,000 in the S&P 500. If you did, you would now have almost $100,000 in 2022. That’s quite an opportunity cost for buying a new car!

Buying too much car is one of the easiest and biggest financial mistakes someone can make. Besides the purchase price of a car, you’ve got to also pay car insurance, maintenance, parking tickets, and traffic tickets.

When you add everything up, I’m pretty sure you’ll be shocked at how much it really costs to own a car and hurl. After more than 10 years, the 1/10th rule for car buying has become the standard car buying rule for financial freedom seekers everywhere.

Mục Lục

The Car Buying Rule To Follow: The 1/10th Rule

The #1 car buying rule to follow is my 1/10th Rule for car buying. The rule states that you should spend no more than 1/10th your gross annual income on the purchase price of a car. The car can be new or old. It doesn’t matter so long as the car costs 10% of your annual gross income or less.

If you make the median per capita income of ~$42,000 a year, limit your vehicle purchase price to $4,200. If your family earns the median household income of $75,000 a year, then limit your car purchase price to $7,500. Absolutely do not go and spend $49,388, the absurdly high average new car price today!

If you absolutely want to buy a car that costs $49,388, then shoot to make at least $493,880 a year in household income. $493,880 is about the top 1% income threshold today.

You might scoff at the necessity to make such a high amount. However, it takes at least $300,000 a year to live a middle class lifestyle with a family today. Inflation has really made making more money necessary just to run in place.

The last thing you want to do is waste money on a car you don’t need.

Minimize Your Financial Stress With A Cheaper Car

If you actually want to save for college, save for retirement, take care of your parents, buy a home, and not stress out about money when you’re old, please keep your car purchase to at most 10% of your annual gross income.

Once you buy a car following my 1/10th rule, own your car for at least five years. Better yet, shoot to own it fo 10 years. Don’t go selling your car every 2-3 years like most Americans do. If you do, you don’t experience the full value of the car. Further, you end up paying wasteful sales taxes each time you buy a new or new used car.

Buying a car you cannot afford is the #1 way to financial mediocrity. One of the biggest benefits of buying a used car is more mental relief. And when you have less stress in your life, you will enjoy it better.

Since Financial Samurai was founded in 2009, my goal is to help readers achieve financial freedom sooner, rather than later. Ideally, I’d like every reader to achieve an above average net worth for their age.

Financial independence is worth it. A car you cannot comfortably afford is a great headwind.

Why You Shouldn’t Spend More Than 10% Gross On A Car

If you want to achieve financial freedom, let’s go through specific reasons why you should follow my 1/10th rule for car buying.

1) Maintenance costs

The more you drive, the more you will pay to maintain your vehicle. With thousands of parts per car, something will inevitably break or need upgrading.

Not only do you have to pay for maintenance costs, you’ve also got to pay for insurance, parking tickets, and traffic tickets. Further, the thrill of owning a new or new used car lasts for only several months. However, the pain of paying the same car payment lasts for years.

2) Opportunity cost

When you buy a car you lose the opportunity of investing your money in assets that will likely grow and pay you dividends in the future. Everybody knows to save early and often to allow for the effects of compounding. Buying too much car is like negative compounding!

Imagine how much money you would have accumulated if you invested $300-$500 a month in the stock market since 2009 instead of paying for a car?

3) More Stress

When you pay more than 1/10th your income for a car, you will become more stressed. You’ll feel stressed whenever you get a door ding after parking your car at the local grocery store. You’ll get stressed whenever you incur wheel rash after parallel parking too close to the curb.

Sometimes when you’re driving in traffic, you’ll feel more on edge because you don’t want anybody damaging your car. If you are within 1/10th of your income, you drive and park stress free. You stop caring about door dings, bumper scrapes, even break ins. Stress kills folks.

4) Makes you want more

The nicer your car, the more you want to spend on other things. You start thinking stupid thoughts like: I’ve got to buy a matching chronometer watch, driving shoes, and outfit. You start paying $20 for valet because you want people to see you come out of your car instead of park for free.

If you think about it, only the rich or fools buy new cars today. With the average new car price at roughly $50,000, a middle-class household should buy used instead.

5) Makes you feel stupid

Deep down, you know that if you can’t pay cash for your car, you can’t afford the car. Each payment you make is a reminder how foolish you are with your money. Why would you want to be reminded every single month of being dumb? The thrill of owning a nice car fades after about six months. But the payment stays the same for years.

Depreciation Chart

Depreciation Chart

If You’ve Already Bought Too Much Car

Look, everybody makes dumb financial moves all the time. The important thing is to recognize your mistake, stop, and fix it! Here are some things you can do if you’ve bought too much car already.

1) Own your car until it becomes worth 10% of your income or less.

This is the simplest solution if you’ve spent too much. Drive your car for as long as possible until the market value is worth less than 10% of your gross annual income.

2) Bite the bullet and sell your car.

If you’ve spent anything more than 1/5th your gross annual income on a car, I’d sell it. It’s making you poor. Even if you have to take a little bit of a hit, I think it’s worth getting rid of your vehicle. Don’t trade it into the dealer because you’ll get railroaded. Instead, try negotiating via Craigslist.

3) Punish yourself.

Like Silas does in The Da Vinci Code, whip yourself into submission! OK, maybe don’t go to that extreme. However, if you don’t punish yourself, then you will repeat your mistake and feel fine with what you have now.

For the life of your car loan, take away a food you love to eat such as chocolate. If you are a coffee addict, swear never to drink that stuff again! Save more of your income after taxes. Feel the squeeze so that you realize how ridiculous your car spending is.

If the amount of money you’re saving each month doesn’t hurt, you’re not saving enough!

Recommended Cars By Income (Tastes May Differ)

The beauty of the 1/10th rule for car buying is that it is tethered to your income. If you want a nicer car, you must make more income! Here are some suggested cars you can buy based on my 1/10th rule.

Cars built in the 1990s and beyond are so much more reliable than those built prior. If you are serious about improving your finances, consider buying a car with less options. The less electronics, the less electrical gremlins too. The more you have loaded in your car, the more maintenance headaches you will have in the future.

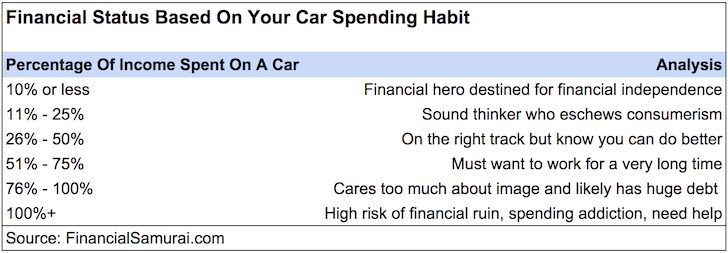

Below is the chart highlighting you financial status based on your car spending as a percentage of household income. The closer you follow my 1/10th rule for car buying, the closer you will get to financial independence.

Please note that there is NO SHAME in owning a car that’s worth less than $10,000. I bought a second-hand Land Rover Discovery II for $8,000. Then I drove it for 10 years until it was worth less than $2,000.

The car was great and loads of fun. With the money saved from not buying a more expensive car, I diligently invested the money. A decade later, the money grew by over 160%. But it is important to pay attention to safety.

In fact, the best time to own the nicest car you can afford is when you have kids. This way, you amortize the cost of the car across more heartbeats. Further, you have more valuable cargo which means a safer car is even more important.

But once you’ve found a safe enough car, put your ego aside so you can have true wealth. All the freedom in the world. Your goal should be to generate enough passive income as possible so you don’t have to work. Be a time millionaire or billionaire! Freedom is the true value of wealth.

The Choice For Great Wealth Is Yours

Treat the 1/10th rule of car buying like a game. You will be surprised to find how many different type of cars you can buy with 1/10th your income if you make over $25,000 a year.

If you want a $30,000 car, get motivated by the 1/10th rule to figure out a way to make $300,000 a year. One way is to start a side hustle to generate more income on the side. We’re all spending way more time at home now. Might as well try to make some side income online.

If you can’t get motivated, then fine. Just don’t think you can afford much more. Think about your future and the future of your family. A car is simply there to take you reliably from point A to point B.

If you’re thinking about prestige and impressing others, don’t be silly. Owning a nice property is way more impressive because at least you can potentially make some money from the asset!

The Worst Combo For Your Finances

One of the worst financial combos is owning a car that you purchased for much more than 1/10th your gross income and renting. You now have two of your largest expenses sucking money away from you every single month.

Think about all the wealthy people you know or the millionaires next door. Chances are high the majority of them own their homes and drive used cars. Their cars likely don’t come close to 50% of their gross income.

If you want to achieve financial independence, follow my 1/10th car buying rule. Letting material things stress you out is no way to live.

If you want to detonate your finances and end up working longer than you want for the sake of a nicer ride, then go ahead and spend more than you can comfortably afford. After all, we’ve only got one life to live.

Recommendations To Build More wealth

1) Track Your Net Worth Religiously

Hopefully you are now motivated to make more money to afford the car of your dreams. Going into debt to buy a depreciating asset is unwise. As you grow your wealth through savings and investments, make sure you stay on top of your net worth.

Sign up for Empower (previously Personal Capital), the best free financial tool on the web. I’ve been using them for free since 2012 and have seen my income and net worth skyrocket. The app keeps me motivated to spend smartly and invest wisely. There is no rewind button in life. Best to get your financial life in order.

Personal Capital’s Free Retirement Planner

Personal Capital’s Free Retirement Planner

2) Invest in real estate

Instead of buying an overpriced car, invest in real estate to build more wealth. Real estate is a core asset class that has proven to build long-term wealth for Americans. Real estate is a tangible asset that provides utility and a steady stream of income if you own rental properties.

Take a look at my two favorite real estate crowdfunding platforms. Both are free to sign up and explore.

Fundrise: A way for accredited and non-accredited investors to diversify into real estate through private eREITs. Fundrise has been around since 2012 and has consistently generated steady returns, no matter what the stock market is doing. For most people, it’s better to invest in a diversified eREIT for exposure and risk management.

CrowdStreet: A way for accredited investors to invest in individual real estate opportunities mostly in 18-hour cities. 18-hour cities are secondary cities with lower valuations and higher rental yields. Further, growth is potentially higher due to job growth and demographic trends. If you have a lot of capital, you can build your own best-of-the-best real estate portfolio.

I’ve personally invested $810,000 in real estate crowdfunding to diversify my exposure and earn income 100% passively. As soon as you realize the opportunity cost of buying a car, you will be more inclined to follow my car buying rule.

The 1/10th Rule For Car Buying is a Financial Samurai original post. I came up with the rule in 2009. If you want to build more wealth, join 55,000+ others and sign up for my free weekly newsletter.

![Toni Kroos là ai? [ sự thật về tiểu sử đầy đủ Toni Kroos ]](https://evbn.org/wp-content/uploads/New-Project-6635-1671934592.jpg)