What to Invest In: Use Your Money to Make Money | The Motley Fool

Investing can be the smartest financial move you make. While you might earn a steady paycheck from working, investing can put your hard-earned money to work for you. A wisely crafted investment portfolio can help you build tremendous wealth over time that you can use for your retirement, to send your kids to college, or for any other financial goals you might have.

Image source: The Motley Fool

However, while it’s fairly common knowledge that investing is a good move, there’s also the question of what you should invest in, which is an extremely important piece of the puzzle.

With that in mind, let’s take a closer look at some of the most popular investment vehicles. We’ll discuss the pros and cons of each and examine whether they might fit into your ideal investment strategy. We’ll also take a look at some of the things you probably shouldn’t invest in.

Mục Lục

Why stocks are good investments for almost everyone

Almost everyone should own stocks. That’s because stocks have consistently proven to be the best way for the average person to build wealth over the long term. U.S. stocks have delivered better returns than bonds, savings accounts, precious metals, and most other investment types over the past four decades.

Stocks have outperformed most investment classes over almost every 10-year period in the past century and have averaged annual returns of 9%-10% over long periods of time. To put returns like this into perspective, a $10,000 investment compounded at 10% for 30 years would grow to nearly $175,000.

Why have U.S. stocks been such great investments? Because as a stockholder, you own a business. And as that business gets bigger and more profitable, and as the economy grows, you own a business that becomes more valuable. As legendary investor Warren Buffett puts it, investing in U.S. stocks is a bet on American business, and this has been an excellent bet for more than two centuries.

We can use the past 20 years as an example. Even across three of the most brutal stock market declines in history, the stock market has delivered better returns than gold or bonds. Consider the benchmark S&P 500 index, widely considered to be the best barometer of how large U.S. stocks are performing. Over the past two decades, the S&P 500 has delivered 540% total returns, which includes stock price gains as well as dividends. In other words, a $10,000 investment would have turned into $64,000, and that’s including the effects of the 2008 financial crisis, COVID-19 crash in 2020, and the bear market downturn of 2022.

The downsides of investing in stocks

Stocks are not a risk-free investment by any definition. Even the most stable companies’ stocks can fluctuate dramatically over short periods of time. Looking back at the past 50 years, the S&P 500 has declined by as much as 37% in a single year and has risen by as much as 38%.

Because of their tremendous wealth-building potential, stocks should make up the foundation for most people’s portfolios. What varies from one person to the next is how much stock makes sense.

Want to compare brokerages?

Browse top stock brokerages

For example, someone in their 30s saving for retirement can ride out many decades of market volatility and should own almost entirely stocks. Someone in their 70s should own some stocks for growth; the average 70-something American will live into their 80s, but they should protect assets they’ll need in the future by investing bonds and holding cash.

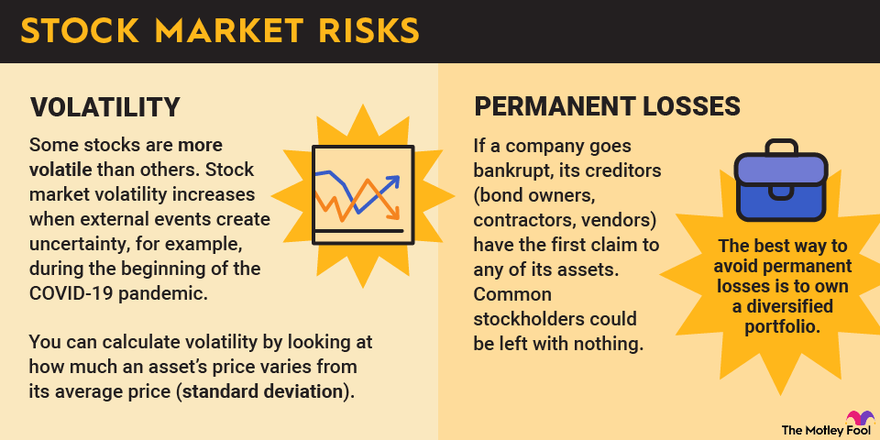

There are two main risks with stocks:

- Volatility: Stock prices can swing broadly over very short periods. This creates risk if you need to sell your stocks in a short period of time.

- Permanent losses: Stockholders are business owners, and sometimes businesses fail. This risk can be mitigated by focusing on established and stable businesses and by creating a diversified portfolio of stocks or choosing to invest in exchange-traded funds (ETFs) or mutual funds.

Managing volatility

If you have a kid heading off to college in a year or two, or if you’re retiring in a few years, your goal should no longer be maximizing growth. It should be protecting your capital instead. It’s time to shift the money you’ll need in the next several years out of stocks and into bonds and cash.

If your goals are still years in the future, you can hedge against volatility by doing nothing. Even through some of the worst market crashes in history, stocks have delivered incredible returns for investors who bought and held.

Avoiding permanent losses

The best way to avoid permanent losses is to own a diversified portfolio, without too much of your wealth concentrated in any one company, industry, or market. Diversification will help limit your losses to a few bad stock picks, while your best winners will more than make up for their losses.

Think about it this way: If you invest the same amount in 20 stocks and one goes bankrupt, the most you can lose is 5% of your capital. Now let’s say one of those stocks goes up 2,000% in value, it makes up for not just that one loser, but would double the value of your entire portfolio. Diversification can protect you from permanent losses and give you exposure to more wealth-building stocks.

Another effective way to avoid permanent losses is to invest (either exclusively or partially) in ETFs and/or mutual funds. For example, if you invest in an S&P 500 index fund, your money will be spread out among the 500 companies that make up the index, and therefore it wouldn’t be devastating if any one of them were to fail.

How much of your money should be in stocks?

To be perfectly clear, every investor is different. There’s no rule of thumb that works for everyone.

Having said that, one popular asset allocation guideline used by financial planners is to subtract your age from 110 to determine the approximate percentage of your portfolio that should be in stocks. For example, according to this rule, a 40-year-old should have roughly 70% of their money invested in stocks.

Why you should invest in bonds

In the previous example, you might be wondering where the other 30% of this hypothetical investor’s money should go. And the general answer is that it should be in stable, income-producing assets, with bonds (or fixed-income securities) being the main category.

Over the long term, growing wealth is the most important step. But once you’ve built that wealth and get closer to your financial goal, bonds, which are loans to a company or government, can help you keep it.

There are three main kinds of bonds:

- Corporate bonds, issued by companies.

- Municipal bonds, issued by state and local governments.

- Treasury notes, bonds, and bills, issued by the U.S. government.

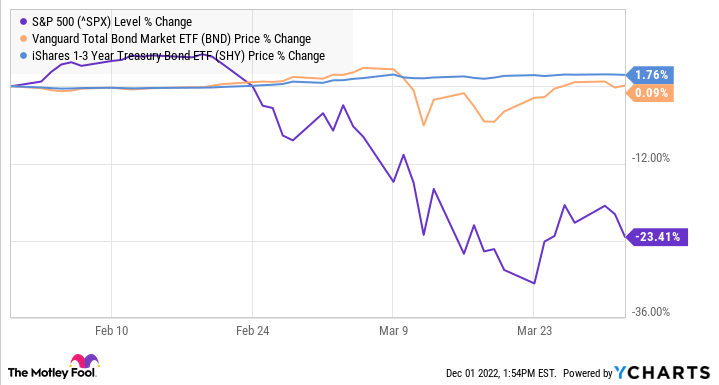

Here is a recent example of how bonds can be useful investments, using the Vanguard Total Bond Market ETF (NYSEMKT:BND), which owns short- and long-term bonds, and the iShares 1-3 Year Treasury Bond ETF (NYSEMKT:SHY), which owns the most stable treasury bonds, compared to the S&P 500. This chart is from February through April 2020, when the COVID-19 pandemic sent financial markets into a panic.

As the chart shows, while stocks were crashing hard and fast, bonds held up much better, because a bond’s worth — the face value, plus interest promised — is easy to calculate and far less volatile.

As you get closer to your financial goals, owning bonds that match up with your timeline will protect assets you’ll be counting on in the short term.

Why and how to invest in real estate

Just like owning great companies, owning real estate can be a wonderful way to build wealth. In most recessionary periods throughout history, commercial real estate has been counter-cyclical to recessions. It’s often viewed as a safer, more stable investment than stocks.

There are ways for people at almost every financial level to invest in and make money from real estate. The most obvious is to buy a rental property, which can be a great way to build wealth and create an income stream, but it isn’t the best fit for everyone.

Fortunately, there are alternative ways to invest in real estate, many of which are much more passive than actually becoming a landlord.

Publicly traded REITs, or real estate investment trusts, are the most accessible way to invest in real estate. REITs trade on stock market exchanges just like other public companies. Here are some examples:

- American Tower (NYSE:AMT) owns and manages communications sites, primarily cell phone towers.

- Public Storage (NYSE:PSA) owns almost 3,000 self-storage properties in the U.S. and Europe.

- AvalonBay Communities (NYSE:AVB) is one of the largest apartment and multifamily residential property owners in the U.S.

REITs are excellent investments for income, since they don’t pay corporate taxes, as long as they pay out at least 90% of net income in dividends.

It’s also easier to invest in commercial real estate development projects now than ever. In recent years, legislation made it legal for real estate developers to crowdfund capital for real estate projects. As a result, billions of dollars of capital has been raised from individual investors looking to participate in real estate development.

It takes more capital to invest in crowdfunded real estate. Unlike public REITs, where you can easily buy or sell shares, once you make your investment you may not be able to touch your capital until the project is completed. There’s also a risk that the developer doesn’t execute, and you can lose money. But the potential returns and income from real estate are compelling and have been inaccessible to most people until recently. Crowdfunding is changing that.

What type of investment account should you use?

Just as owning the right investments will help you reach your financial goals, where you invest can be just as important. Many people, especially newer investors, don’t consider the tax consequences of their investments, which can leave you short of your financial goals.

Simply put, a little bit of tax planning can go a long way. Here are some examples of different kinds of accounts you may want to use on your investing journey:

Table by author.

Investing Account Type

Account Features

Need to Know

401(k)

Pre-tax contributions reduce taxes today. Potential employer-matching contributions.

Distributions in retirement are taxed as regular income. Penalties for early withdrawal. $20,500 employee contribution limit in 2022 ($22,500 in 2023).

SEP IRA/Solo 401(k)

Pre-tax contributions reduce taxes today. Higher contribution limits than IRAs.

Distributions in retirement are taxed as regular income. Penalties for early withdrawal. $61,000 total contribution limit in 2022 ($66,000 in 2023).

Traditional IRA

Use to rollover 401(k) from former employers. Contribute retirement savings above 401(k) contributions.

Distributions in retirement are taxed as regular income. Penalties for early withdrawal. $6,000 contribution limit in 2022 ($6,500 in 2023).

Roth IRA

Distributions are tax-free in retirement. Withdraw contributions penalty-free.

Contributions are not pre-tax. Penalties for early withdrawal of gains. $6,000 contribution limit in 2022 ($6,500 in 2023).

Taxable brokerage

Contribute any amount to your account without tax consequences (or benefits). Withdraw money at any time.

Taxes are based on realized events (even if you don’t withdraw proceeds), i.e., you may owe taxes on realized capital gains, dividends, and taxable distributions.

Coverdell Education Savings Account

More control over investment choices. Withdrawals for qualified education expenses are tax-free.

$2,000 annual contribution limit; further limits based on income. Taxes and penalties for nonqualified withdrawals.

529 College Savings

Withdrawals for qualified education expenses. Very high contribution limits.

More complicated, varying by state. Fewer investment choices. Taxes and penalties for nonqualified withdrawals.

The biggest takeaway here is that you should choose the appropriate kind of account based on what you’re investing for. For instance:

- 401(k): For employed retirement savers

- SEP IRA/Solo 401(k): For self-employed retirement savers

- Traditional IRA: For retirement savers

- Roth IRA: For retirement savers

- Taxable brokerage: For savers with additional cash to invest beyond retirement/college savings account needs or limits

- Coverdell Education Savings Account: For college savers

- 529 College Savings: For college savers

Related investing topics

More points to keep in mind based on why you are investing:

- Maximize employer-sponsored retirement plans, like 401(k) plans, at least up to the maximum amount your employer will match.

- If your earnings allow you to contribute to a Roth IRA, building up tax-free income in retirement is an excellent way to help secure your financial future.

- Using the Roth-like benefits of the Coverdell and 529 college savings plans removes the tax burden, resulting in more cash to pay for education.

- A taxable brokerage account is an excellent tool for other investing goals, or extra cash above retirement account limits.

The bottom line is that everyone’s situation is different. You must consider your investment time horizon, desired return, and risk tolerance to make the best investment decision to reach your financial goals.

Matthew Frankel, CFP® has positions in Public Storage. The Motley Fool has positions in and recommends American Tower. The Motley Fool recommends AvalonBay Communities. The Motley Fool has a disclosure policy

![Toni Kroos là ai? [ sự thật về tiểu sử đầy đủ Toni Kroos ]](https://evbn.org/wp-content/uploads/New-Project-6635-1671934592.jpg)